80C – Save Tax + Create Wealth [Updated post Budget 2021]

We are in the last quarter of the financial year 2020-2021. It sounds a little odd since most of us finished filing our Income tax returns for FY 19-20 just a few days back.

2020 was a crazy year and we got extensions for all statutory compliances. But I doubt the Government will be as open-handed in 2021. Most of the due dates will not be extended.

For example, to claim deduction under section 80C of the Income Tax Act, 1961 you have to make investment on or before 31st March of the relevant financial year. Last year, the Government extended the due date till 31st July, 2020. I don’t think we will see any extension this year. So that leaves a little less than 2 months to plan, evaluate, curate and execute your 80C investments.

- First of all what is Section 80C?

Section 80C of the Income Tax Act, 1961 intends to promote and encourage the habit of saving/investing amongst citizens. The Government has listed a few types of investments that are eligible under this section. The amount that you invest in any of these eligible investments is deducted from your taxable income. The maximum deduction benefit you can claim under this section is Rs. 1,50,000.

[An additional deduction limit of Rs 50,000 u/s 80 CCD is available for investments in the National Pension Scheme. But NPS is an exceptionally complex product and we will save it for some other day].

Let’s say your taxable income is Rs 15 lakhs and you invest in Rs 1 lakh in an investment eligible u/s 80C. In that case, you will have to pay tax on Rs 14 lakhs only. In this example your marginal rate of tax will be 30%, so, you saved Rs 31,200 (including 4% cess) straight away. Had you invested up to the full limit of Rs 1,50,000 you would have saved Rs 46,800/-.

- What is the need for section 80C?

Like I mentioned earlier, the Government intends to promote and encourage the habit of saving/investing amongst citizens. In order to save tax, people will invest their money instead of keeping it idle or spending it away. This will help in creating a corpus which can be used for securing your retirement life.

- What types of investments are eligible u/s 80C?

Bitcoins, Emu eggs, Tulips? NOOO! You can’t invest in any of these.

The idea is to secure your future not punt it on some speculative bubble. More or less, these are the features of an 80C investment:

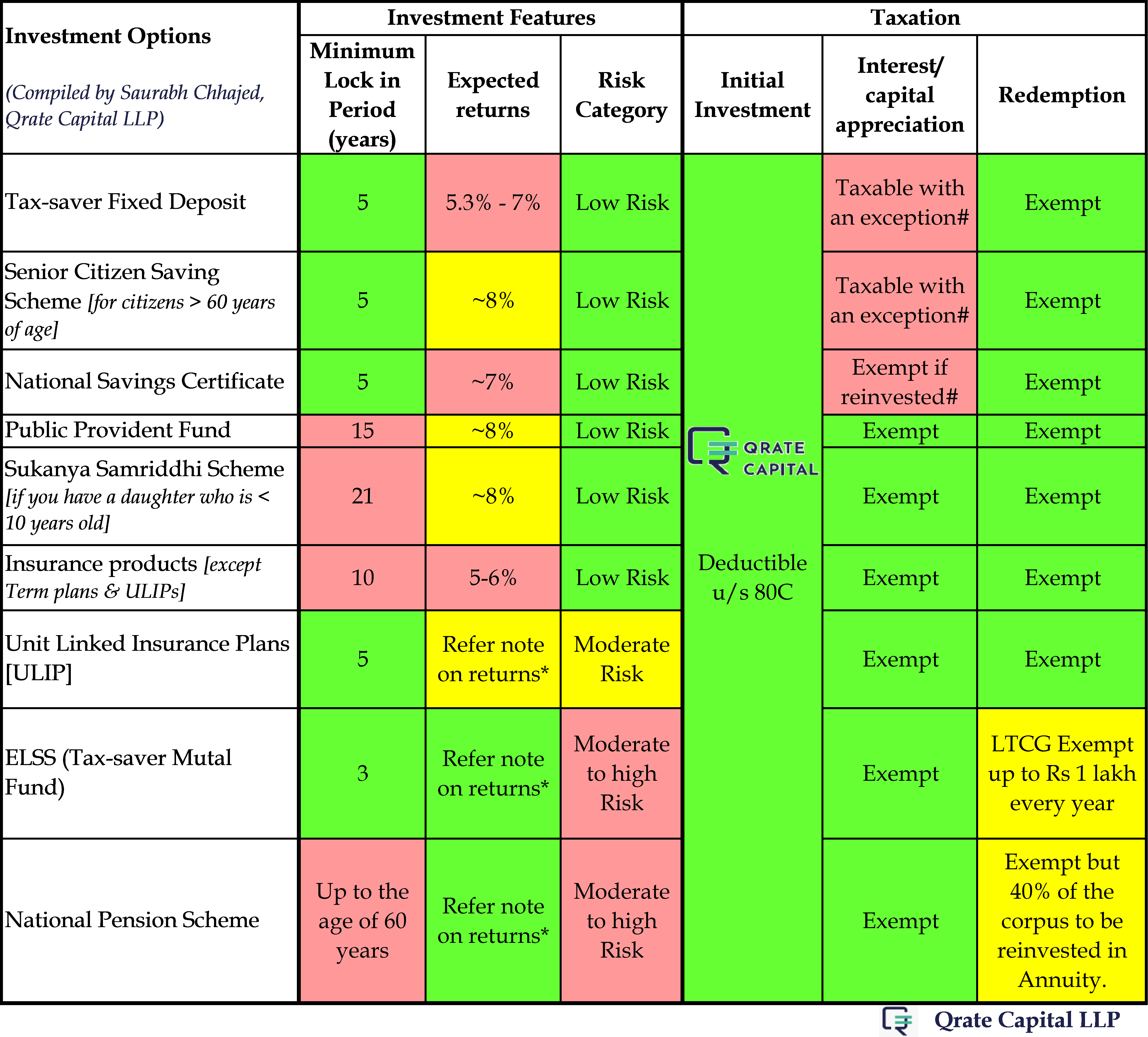

- Lock-in period – All investments cannot be redeemed for a certain pre-designated period of time. This ensures a forced discipline and prevents from pre-mature redemption.

- Reasonable returns – Do not expect superlative returns. [ELSS might give spectacular returns for a limited period but they also under-perform at times.] Having said that, some of them have the ability to deliver returns higher than the inflation.

- Low to moderate risk – Some products carry very low risk while a product like ELSS carries moderate risk.

- There are certain expenditures/deductions that can be claimed u/s 80 C – like –

- Premium paid on term life insurance

- Principal repayment of your housing loan

- EPF deducted from your salary by your employer [Employee (not employer) contribution to EPF]

- Stamp duty paid on purchase of a house, etc.

If these do not max out your 80C then you have the below options that you can choose from:

* Note on Returns:

NPS, ULIPs and ELSS do not offer guaranteed returns. Their returns are Market-linked (stock market, debt market, etc). Thus, returns are volatile – they are spectacular in some years and pathetic (even negative) in some years.

If you invest for a period of 5 years in these 3 investments, how much CAGR (compounded annual growth rate) can you expect?

NPS – 9-10%; ULIP – 7-8%; ELSS – 10-12%

These are merely estimates based on median historical performance. Actual returns may be higher or lower in the future.

- Note on Taxation

For the purpose of Income Tax Act, 1961 there are 3 stages to this transaction. The law has clearly defined whether an income tax liability will arise at any stage of the transaction. [Disclaimer – Laws are subject to change at the discretion (whims and fancies) of the Government].

Stage 1 – Initial investment

When you invest the money, you get a deduction from income tax. This is true for all the above investments. [That’s why they are in the list, duh!].

Stage 2 – Returns on Investment

Returns on investment can be in the form of Interest / Capital Appreciation.

- For market-linked investments like NPS, ULIP and ELSS returns are in the form of capital appreciation, i.e. the value of your investment goes up/down along with the underlying assets. For other options, returns are in the form of interest.

The returns earned are exempt from tax except:

- # NSC – Interest is taxable but

Interest is cumulative, i.e. it is calculated annually but paid only at maturity. The annual interest is deemed to be reinvested u/s 80C subject to availability of Rs 1.5 lakhs limit. The interest is first added to your income. Then if you have unutilised limit u/s 80C you can claim deduction for reinvested interest and reduce your income.

Simply put, if you are someone who likes to max out the 80C limit, the interest is as good as taxable for you.

- # Senior Citizen Saving Scheme & Tax-saver Fixed Deposit – Interest is taxable but

There is a section 80TTB which says that a senior citizen (>60 years) earning interest from deposits with banks or post offices need not pay tax on such interest up to Rs. 50,000. Interest portion above the Rs 50,000 limit is fully taxable.

Stage 3 – Redemption

Redemption proceeds are mostly exempt except –

- ELSS: Long Term Capital Gains on sale of listed equity shares or units of mutual funds up to Rs 1 lakh are exempt every year.

Let’s say you invest Rs 1.5 lakhs in 2014 and when you redeem in 2020 you get an amount of Rs 2.7 lakhs. Thus, your capital gain = 1.2 lakhs [2.7 (less) 1.5]

Exemption up to Rs 1 lakh is available every year. So, you have to pay tax only on Rs 20,000 at a flat rate of 10% (+cess) irrespective of your slab rate.

- ULIPs: Redemption on death of the policy holder is Exempt in all cases.

For Redemption in cases other than deaths: Policies issued on or before 31.01.2021 – Exempt.

For policies issued on or after 01.02.2021 – Exemption only for policies where the total premium payable in any year does not exceed Rs 2.5 lakhs during the term of the policy.

Let’s say:

| Policy | 1 | 2 | 3 | What should you do? |

| Annual Premium (Rs) | Rs 1 lakhs | Rs 50,000 | Rs 1.4 lakhs | Claim Exemption for Policy 1 and 3, Pay Tax for Policy 2 |

Now comes the most important part – How do you choose?

All the options have pros as well as cons.

I suggest “Selection by Elimination”.

Are you above 60 years of age?

Most likely, you are not (I know my audience). So, Senior Citizen Savings Scheme is not even an option for you. Plus, you cannot claim benefit u/s 80TTB so that makes Tax-saver FDs a lot less desirable as the interest earned will be fully taxable.

What about NSC?

Like I said if you are someone who likes to max out the 80C limit, it is as good as taxable for you. NSCs are better than Tax-saver FDs because they pay a higher rate of interest but they score very low on “ease of investing” score. For everything – investing, updating your passbook, redeeming – you have to visit the Post Office. You cannot do anything online.

Public Provident Fund & Sukanya Samriddhi Scheme

Frankly, there is nothing to choose in terms of features. PPF is more broad-based in terms of who is eligible to invest and its rules for partial withdrawal. [Personally, if I have to choose one fixed income investment for the long-term, I would select PPF over any other currently available option.]

Insurance products [except Term plans] & ULIPs

I firmly believe that insurance and investments need to be kept separate. If you mix them, you end up with a lousy investment and an insufficient insurance cover.

Poor Returns – Returns in traditional insurance products and ULIPs are lower than their peers in the fixed income category and market-linked category respectively by a good 2%.

Insufficient Insurance – As far as insurance cover is concerned, it is generally 10x of the annual premium. If you pay a premium of Rs 1,00,000 (x) per year, you will likely get an insurance cover of Rs 10 lakhs (10x). You think that’s enough for your family?

Traditional Insurance Products – You get a return which is more or less the same as the ongoing FD rate, the insurance cover is significantly short of what you need and you get locked for 10 years or more! I would much rather invest in PPF and earn a 2% higher return rather than run behind that paltry insurance cover. A 2% higher return over a period of 10-15 years makes a huge difference in your redemption proceeds.

ULIPs – Let’s say you want to invest Rs 1 lakh per year in ULIPs. You are better off investing 70-80k in ELSS and use another 20-30k to buy a term plan. You will sleep peacefully at night knowing that your family’s finances are secure in case of an unforeseen event. Your investment too will be well placed to outperform other options.

After the recent changes in Budget 2021, taxation advantage that ULIPs enjoyed on redemption over ELSS redemption has also reduced .

Insurance companies have a great sales pitch for these products. I have seen many gullible investors fall prey to these rosy sales pitches. You have been warned.

Last but not the least – ELSS

I think I don’t need to say much about mutual funds. They are the best option if you are looking to create long-term wealth and have time on your side. You still need to be careful about the fund you choose. I know there are dozens of funds and it is difficult to decide. Don’t worry; you can reach out to us! Contact details are in the footer.

For more informative articles, follow our LinkedIn Page – https://www.linkedin.com/company/qrate-capital-llp

P.S. The article has been updated to reflect the recent changes in taxation law. Thus, some information will differ from the original article – 80C – Save Tax + Create Wealth which was published on 09/01/2021on.