Growth Vs Dividend Options in Mutual Funds – Which one should you choose?

Saurabh, why do you always recommend Growth option in Mutual funds?

What is this Dividend option? Do we get a dividend from the Mutual Fund? Isn’t that great?

I get these questions a lot. So, here’s the deal about Growth Vs Dividend option in mutual funds.

What is Dividend?

A dividend is the distribution of some part of a company’s profits to its shareholders.

I have purposely emphasised the word “profits”. We will come to this in the latter half of the blog.

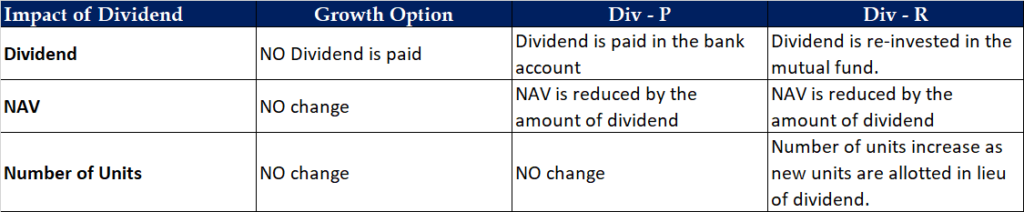

What Variants (Options) are available in any Mutual Fund Scheme?

A Mutual Fund Scheme can offer 3 options to its investors. So, let’s assume an XYZ Equity Fund with 3 variants was started on 01/01/2021 with all 3 variants having an NAV of Rs 10 per unit.

- XYZ Equity Fund – Growth option [Let’s call this “Growth” option]

- XYZ Equity Fund – Dividend Payout option [Let’s call this “Div – P” option]

- XYZ Equity Fund – Dividend Reinvestment option [Let’s call this “Div – R” option]

The Fund Manager, investing strategy and the portfolio will be the same in all 3 variants. Everything is same except one small detail – XYZ equity fund has decided to pay a monthly dividend of Rs 0.1 per unit.

Let’s assume that you invested Rs 10 lakhs in the fund on 01/01/2021. Thus, you got 1,00,000 units at an NAV of Rs 10 per unit. What difference will the dividend make in the 3 variants?

Growth Option – You will not be paid any dividends.

Div – P option – Dividend will be credited to your bank account. But the NAV of the fund will be reduced by an equal amount. So, if the dividend amount is Rs 0.1 per unit, your NAV will be reduced by Rs 0.1 per unit. So, what you gain via dividend that you are paying back in the form of reduction in NAV.

Div – R Option – You are eligible for dividend but you will not receive the dividend in your bank account. Instead, the dividend will be re-invested in XYZ Equity Div – R scheme. NAV will be reduced by the Dividend amount but number of units will increase. Effectively, the quantum of your investment remains the same.

You get paid in one pocket (dividend) which is taken away from another pocket (NAV reduction). So, it’s all the same. Why are we even discussing it?

Because – Never Forget Taxes!

Dividend is taxed at your slab rate. So, if you fall under the 30% slab rate, you will have to pay 30% tax on your dividend income.

Whereas, profits on sale of Equity MF investment, are classified as Capital Gains. Short-term capital gains are taxed at @15% and long-term capital gains are taxed at 10% irrespective of your slab rate. Please note that taxation rules are different for Debt Mutual Funds. Below illustration is for Equity Mutual Funds.

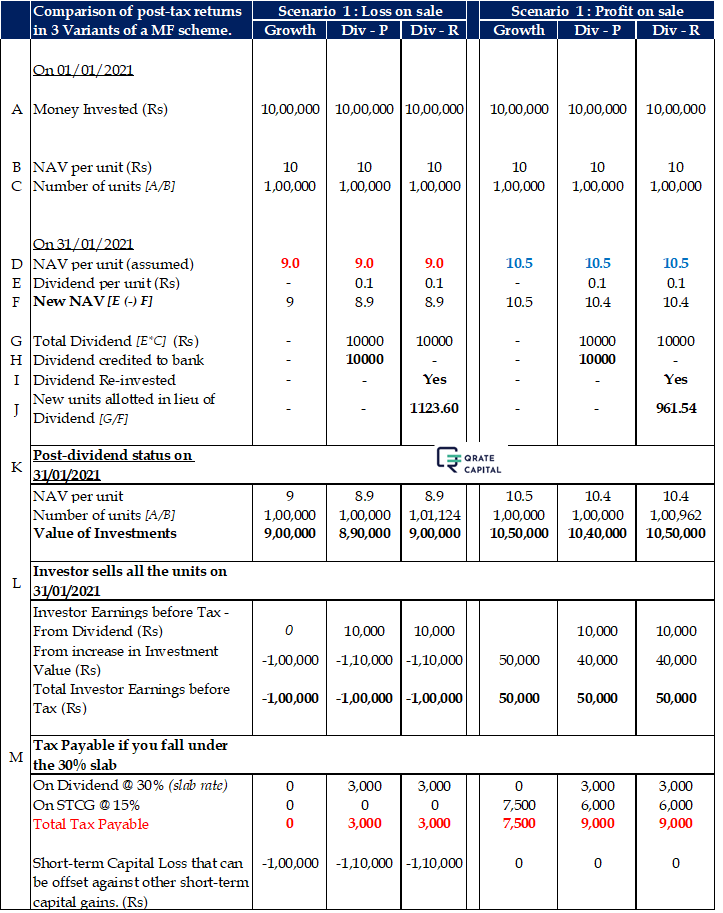

Also, there is a fundamental difference in how dividends are paid by a mutual fund. In any other case, dividends are paid only if there are profits. In a mutual fund, dividend is paid even if there is a loss. That basically means that what is paid in the form of dividend is actually your capital being returned to you. So, imagine a scenario where –

- You invested Rs 10,00,000 in Div – P or Div – R option.

- The value has fallen to Rs 9,00,000 because the stock market is having a bad time.

- The fund pays you a dividend of Rs 10,000.

How can it pay a dividend when there is no profit? It is actually returning your capital to you and that too at a 10% loss. What’s worse? You have to pay tax on this Rs 10,000. So, you are paying tax on your losses as well. Absurd!

Annexure 1 at the end of the blog exposes the inefficiency of Dividend options.

There is another extremely important factor that works in favour of “Growth” option – Compounding!

If you keep reducing your invested corpus (via dividends or otherwise), how will you give your portfolio the chance to take benefit of compounding?

An important question that may be raised –

What about someone who wants to invest in a mutual fund but is also looking for a small monthly inflow to take care of a few small expenses?

That’s where we recommend a combination of SWP and Asset Allocation techniques. There are 3 objectives of this strategy –

- ensure the investor gets a monthly cashflow;

- ensure that only the debt portion is pinched in the short-term while the equity portion gets a long enough time to grow in value; and

- ensure that tax impact is minimised.

Anyways, even SEBI has woken up and realised the term Dividend is misleading for MF variants. It has mandated that w.e.f. 01/04/2021 – “The dividend payout option will be renamed as Payout of Income Distribution cum capital withdrawal option, dividend re-investment will be renamed as reinvestment of Income distribution cum capital withdrawal plan”.

Better Late Than Never.

#MutualFunds #GrowthVsDividendinMF #FinancialPlanning

You can Connect with us on – LinkedIn & Facebook

Or read our blogs on the website – https://qratecapital.com/blog

Annexure 1

Growth vs Dividend – Numbers expose the tax inefficiency of Dividend option

If you have any views/queries, let us know in the comments.